Can You Claim Back Overpaid National Insurance?

- MAZ

- Mar 29, 2024

- 18 min read

Updated: Mar 26

Understanding National Insurance Overpayments and Eligibility

Yes, you can claim back overpaid National Insurance (NI) contributions in the UK if you’ve paid more than required due to errors, multiple jobs, or other specific circumstances. National Insurance funds critical benefits like the State Pension and NHS, but overpayments can slip through the cracks, leaving taxpayers out of pocket. HMRC processes NI refund claims each year. Refer to GOV.UK for the latest available statistics.. This part breaks down why overpayments happen, who’s eligible, and what’s at stake.

Why Do NI Overpayments Happen?

Now, let’s get to the nitty-gritty: overpayments often stem from how NI is calculated. Unlike income tax, which is cumulative over the year, NI is deducted per pay period (weekly or monthly) without always considering your total annual earnings. This can lead to errors, especially if your work situation is less than straightforward. Common culprits include:

Multiple Jobs: Each employer deducts Class 1 NI independently, potentially pushing you over the annual maximum (approximately £3,016 if earnings exceed £50,270).

Post-State Pension Age: You shouldn’t pay Class 1 or Class 4 NI after reaching State Pension age (66 in 2025), but payroll errors can persist.

Employed and Self-Employed: Paying both Class 1 and Class 4 NI can exceed the annual cap.

Employer Mistakes: Incorrect tax codes or payroll data can inflate deductions.

Voluntary Contributions: Overpaying Class 2 or Class 3 NI when not needed (e.g., already qualifying for full State Pension).

Be careful! HMRC doesn’t proactively check your NI record for overpaid contributions, so it’s on you to spot mistakes.

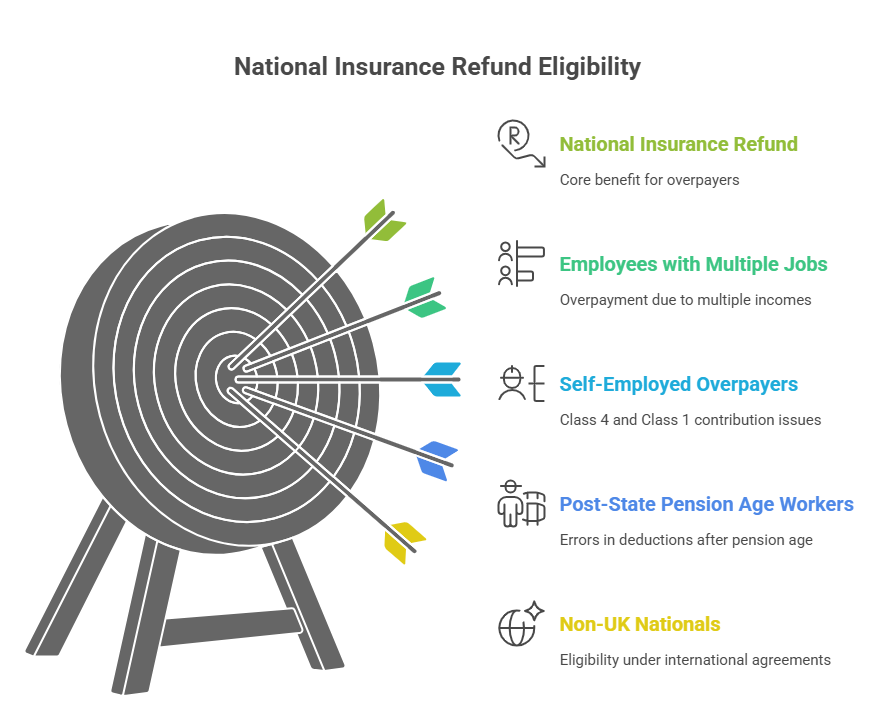

Who Can Claim a Refund?

So, who’s in the driver’s seat for a refund? If you fall into these categories for the 2026/27 tax year, you might be eligible:

Employees with Multiple Jobs: Total earnings above £50,270 (Upper Earnings Limit) but NI deducted on each job.

Self-Employed Overpayers: Paid Class 4 NI on profits above £12,570, especially if also paying Class 1.

Post-State Pension Age Workers: Class 1 or Class 4 NI deducted after age 66.

Non-UK Nationals: Paid Class 1 NI during short-term UK work (e.g., 52-week secondments) under specific conditions.

Voluntary NI Payers: Paid Class 3 NI unnecessarily (e.g., already have 35 qualifying years for State Pension).

Now, here’s a quick reality check: you can’t claim a refund just because you stopped working mid-year or left the UK, unless specific criteria apply (e.g., working abroad under a double taxation agreement).

What Are the NI Classes and Rates for 2026/27 ?

None of us is a tax expert, but understanding NI classes is key to spotting overpayments. Here’s a breakdown for the 2026/27 tax year, sourced from GOV.UK:

NI Class | Who Pays | Rate/Threshold (2026/27) | Purpose |

Class 1 | Employees | 8% on earnings £12,570–£50,270; 2% above £50,270 | State Pension, benefits |

Class 2 | Self-employed | Voluntary (£3.45/week if profits < £6,845) | State Pension (treated as paid if profits ≥ £6,845) |

Class 4 | Self-employed | 6% on profits £12,570–£50,270; 2% above £50,270 | No benefits, tax-like |

Class 3 | Voluntary | £17.45/week | Boost State Pension |

Now consider this: If you’re paying Class 1 and Class 4 simultaneously, your total NI might exceed the annual maximum, making you eligible for a refund. Check your payslips or Self Assessment records to confirm.

How Much Could You Be Owed?

Let’s talk numbers. Say you’re Gwilym, a 40-year-old Cardiff-based graphic designer earning £35,000 from a PAYE job and £25,000 from freelance work in 2026/27. Each employer deducts Class 1 NI at 8% on earnings between £12,570 and £35,000, totaling £1,834 per job. You also pay Class 4 NI at 6% on £25,000 profit, adding £750. That’s £4,418 total, but the annual NI cap is around £3,496 for earnings above £50,270. Gwilym could claim back roughly £922, assuming no deferment was applied.

Now, don’t get too excited—refunds depend on your exact earnings and NI class. Use HMRC’s online NI checker via your Personal Tax Account to estimate overpayments.

Does Overpaying NI Affect Your State Pension?

Here’s a common worry: does overpaying NI mess with your pension? Good news—it doesn’t. Overpayments don’t reduce your qualifying years (35 needed for full State Pension). However, paying unnecessary voluntary Class 3 NI (e.g., if you already have 35 years) won’t boost your pension either. Check your NI record on GOV.UK to avoid this trap.

How to Identify and Claim Back Overpaid National Insurance

Now that you know why National Insurance (NI) overpayments happen and who’s eligible, let’s dive into the practical stuff: figuring out if you’ve overpaid and getting your money back. This part walks you through spotting overpayments, the step-by-step process to claim a refund, and some lesser-known scenarios that could put cash back in your pocket. With HMRC processing over £500 million in NI refunds in 2024/25 (per GOV.UK estimates), there’s no reason to miss out.

How Can You Tell If You’ve Overpaid NI?

So, the question is: how do you know if you’re owed a refund? Overpayments aren’t flagged automatically, so you’ll need to do some detective work. Start with these steps:

Check Your Payslips: Look for Class 1 NI deductions, especially if you have multiple jobs. Compare total deductions against the 2026/27 NI thresholds (£12,570–£50,270 at 8%, 2% above).

Review Your P60 or P45: These show annual NI contributions. If you’ve paid more than £3,496 (the approximate cap for high earners), you might be overpaying.

Log into Your Personal Tax Account: HMRC’s online portal shows your NI record and contributions. Cross-check with your earnings.

Self-Employed? Check Self Assessment: Class 4 NI is calculated on profits. If you also pay Class 1, use HMRC’s NI calculator to check for overlap.

Post-State Pension Age?: If you’re 66 or older and still see Class 1 or Class 4 deductions, you’ve likely overpaid.

Be careful! Don’t rely on your employer to catch errors—payroll mistakes are common, especially with zero-hours contracts or agency work.

What Documents Do You Need to Claim a Refund?

Now, let’s get organised. To claim back overpaid NI, you’ll need solid evidence. Here’s what HMRC typically asks for, based on 2026/27 guidance:

P60 or P45: For employees, showing annual NI contributions.

Payslips: To verify Class 1 deductions, especially for multiple jobs.

Self Assessment Records: For Class 4 or Class 2 NI proof.

Bank Details: For HMRC to process your refund.

NI Number: Essential for all claims.

Form CA5610 or CA8480: For specific cases like post-State Pension age or employed/self-employed overlaps.

None of us loves paperwork, but having these ready speeds things up. Scan or photocopy everything before sending to HMRC.

Step-by-Step Guide to Claiming Your NI Refund

Right, here’s the meat and potatoes: how to actually get your money back. Follow this guide for a smooth process, tailored to 2026/27 rules:

Verify Overpayment: Use your Personal Tax Account or HMRC’s NI checker to confirm you’ve paid too much.

Contact HMRC: Call 0300 200 3500 or write to National Insurance Contributions Office, HMRC, BX9 1AN. Explain your situation (e.g., multiple jobs, post-State Pension age).

Complete the Right Form:

CA5610: For overpayments due to multiple jobs or employed/self-employed status.

CA8480: For post-State Pension age overpayments.

Self Assessment Adjustment: For Class 4 overpayments, amend your tax return.

Submit Evidence: Send copies of P60, payslips, or Self Assessment records. Include your NI number and bank details.

Wait for Processing: HMRC typically takes 6–12 weeks to review claims. You’ll get a letter or bank transfer if approved.

Chase Up if Delayed: If no response after 12 weeks, call HMRC again.

Now consider this: If you’re claiming for previous years (up to 6 years back, e.g., 2019/20–2024/25), use the same process but expect extra scrutiny. HMRC’s deadline for 2019/20 claims is 5 April 2026.

How Long Does an NI Refund Take?

Let’s be real—nobody likes waiting for money. In 2025, HMRC’s processing time for NI refunds averages 8 weeks, though complex cases (e.g., non-UK nationals) can take up to 16 weeks. If approved, refunds are paid via bank transfer or cheque. To avoid delays, double-check your forms and keep copies of all correspondence.

Can Non-UK Nationals Claim NI Refunds?

Here’s a curveball: what if you’re not a UK citizen? Non-UK nationals working in the UK (e.g., on a 12-month visa) can overpay NI, especially under PAYE. You might be eligible for a refund if:

You worked under a double taxation agreement (e.g., EU/EEA countries).

You paid Class 1 NI but left the UK before qualifying for benefits.

You overpaid due to incorrect tax codes (common for short-term workers).

For example, Priya, an Indian software developer, worked in London for 9 months in 2024/25, earning £40,000. Her employer deducted £2,174 in Class 1 NI, but she left the UK permanently. Under India’s tax treaty, she reclaimed £1,800 after proving her departure. Contact HMRC’s International Tax team for these claims.

Can You Claim NI Refunds After Leaving the UK?

Now, if you’ve left the UK, things get trickier. You can claim a refund if you overpaid NI while working in the UK, but only for specific reasons (e.g., multiple jobs, post-State Pension age). Use form CA8480 or write to HMRC with your NI number, UK address (if any), and proof of overpayment. If you worked in an EEA country afterward, check if NI contributions transfer under EU rules.

How to Prevent Future NI Overpayments?

So, how do you avoid this hassle next year? Prevention is better than a refund chase. Try these tips:

Apply for NI Deferment: If you have multiple jobs or are employed/self-employed, use form CA72A to cap your NI contributions.

Check Your Tax Code: If over 66, ensure your employer uses the “NP” category letter.

Monitor Your NI Record: Check your Personal Tax Account annually.

Update HMRC: Notify HMRC of changes (e.g., stopping self-employment) to adjust Class 2/4 payments.

For instance, Dafydd, a Bristol-based electrician, applied for deferment in 2024/25 after overpaying £700 in 2023/24. His Class 4 NI was reduced, saving him time and stress.

A Detailed Step-by-Step Guide to Claiming Back Overpaid National Insurance

Navigating the complexities of National Insurance (NI) contributions can sometimes result in overpayments. Understanding how to claim back these overpayments is crucial for individuals to ensure they are not financially disadvantaged. This comprehensive guide provides a step-by-step approach to reclaiming overpaid National Insurance in the UK, ensuring that you can manage this process effectively and efficiently.

Step 1: Determine If You Have Overpaid

Identify the Causes of Overpayment

Overpayments can occur due to several reasons:

Incorrect NI category applied.

Change in employment status not updated.

Errors in payroll processing by your employer.

Contributions made both as an employee and self-employed simultaneously exceeding the maximum limit.

Check Your Payslips

Regularly review your payslips to verify the accuracy of the NI deductions. Look for any discrepancies in the NI category codes or the amounts deducted.

Step 2: Gather Required Documentation

Collect Necessary Documents

To prepare for a claim, gather the following:

Payslips showing NI deductions.

P60 or P45 forms received from your employer.

Employment history details if you’ve had multiple jobs within the same tax year.

Details of any self-employed contributions if applicable.

Record Keeping

Ensure all documents are organised and easily accessible. This documentation will support your claim and may be required by HM Revenue and Customs (HMRC).

Step 3: Contact Your Employer

Before reaching out to HMRC, discuss the discrepancy with your employer. Often, errors can be rectified internally. Your employer can adjust the overpayment in your future NI contributions or issue a refund directly.

Step 4: Reach Out to HMRC

If your employer cannot resolve the issue, your next step is to contact HMRC directly.

Contact Details

Use the following contact methods:

HMRC’s National Insurance helpline.

Online through your Government Gateway account.

By writing to HMRC’s National Insurance Contributions office.

Provide them with your National Insurance number, detailed employment history, and copies of any relevant documents.

Step 5: Fill Out the Relevant Forms

HMRC may require you to complete specific forms depending on the nature of your claim:

CA5403 ‘Your National Insurance Record’

Fill out this form to get a complete record of your NI contributions, which can help identify any anomalies.

Claim Forms for Specific Cases

For instance, if you’ve made contributions in both employment and self-employment, different forms might be required to address each category.

Step 6: Review HMRC’s Response

After submitting your claim, HMRC will review your case and respond. This process can take several weeks.

Possible Outcomes

Adjustment of Future Contributions: If you continue in the same employment, HMRC might adjust future contributions to correct the overpayment.

Refund: If an immediate refund is warranted, HMRC will issue a cheque or direct bank transfer.

Further Information Required: HMRC may request additional information or clarification.

Step 7: Appeal If Necessary

If you disagree with HMRC’s decision, you have the right to appeal.

Appeal Process

Follow these steps for the appeal:

Request a formal review from HMRC.

If unresolved, escalate to the independent tax tribunal.

Make sure to adhere to any deadlines provided for appeals to ensure your case is heard.

Step 8: Monitor and Prevent Future Overpayments

Regular Checks

Regularly check your NI contributions via payslips and your personal tax account online. This monitoring helps avoid future overpayments.

Educate Yourself

Understand the different NI categories and rates applicable to your employment status. This knowledge can help you identify errors more promptly.

Reclaiming overpaid National Insurance contributions involves a clear understanding of your NI records, diligent record-keeping, and proactive communication with your employer and HMRC. By following these detailed steps, individuals can ensure they manage their contributions effectively, claim any overpayments, and prevent future errors. This process not only secures your financial interests but also deepens your understanding of the UK's tax system, empowering you to take control of your financial responsibilities.

Practical Tips and Key Takeaways for NI Refunds

Now, let’s wrap things up with some real-world advice and a clear summary of the most critical points about claiming back overpaid National Insurance (NI) in the UK. This part dives into advanced strategies, common pitfalls, and rare scenarios to help you maximise your refund and avoid future overpayments. Whether you’re a taxpayer juggling multiple jobs or a business owner navigating Self Assessment, these insights will keep you in control of your NI contributions for the 2026/27 tax year.

What Are the Common Mistakes to Avoid When Claiming NI Refunds?

Let’s be honest—dealing with HMRC can feel like navigating a maze. One wrong turn, and your refund could be delayed or denied. Here are the top mistakes to steer clear of:

Missing Deadlines: You can claim refunds for up to 6 years back (e.g., 2019/20 claims are valid until 5 April 2026). Miss this, and your money’s gone.

Incomplete Documentation: Sending a claim without P60s, payslips, or your NI number is a recipe for rejection.

Ignoring Tax Codes: If your employer uses the wrong tax code (e.g., not accounting for State Pension age), NI deductions won’t stop automatically.

Not Checking NI Records: Assuming your contributions are correct without verifying via your Personal Tax Account can cost you.

For example, Sioned, a Swansea-based nurse, nearly lost a £600 refund for 2022/23 because she didn’t submit her P45. A quick call to HMRC and resubmission saved the day.

How Can Business Owners Avoid NI Overpayments?

Now, if you’re a business owner, NI can be a headache, especially if you’re both employed and self-employed. Class 4 NI (6% on profits £12,570–£50,270) often overlaps with Class 1 if you’re also on PAYE. To stay ahead:

Apply for Deferment Early: Use form CA72A to limit Class 1 or Class 4 contributions if your total NI exceeds the annual cap (£3,496 for 2026/27).

Track Profits Monthly: Use accounting software like Xero to monitor profits and estimate Class 4 NI.

Consult an Accountant: For complex cases (e.g., fluctuating profits), a tax expert can spot overpayments early.

Take Rhys, a self-employed plumber in Newport. In 2024/25, he paid £1,200 in Class 4 NI on £30,000 profits and £1,834 in Class 1 NI on a £35,000 part-time job. After applying for deferment, he reclaimed £900 and adjusted future payments.

What About Rare Scenarios Like Zero-Hours Contracts or Working Abroad?

Now consider this: some situations are less common but just as important. If you’re on a zero-hours contract, NI deductions can fluctuate wildly due to irregular pay. Check your payslips monthly to catch overpayments early. For example, Aneurin, a Manchester-based retail worker, overpaid £400 in 2023/24 because his agency didn’t adjust his NI for low-earning weeks.

If you’ve worked abroad, NI refunds get trickier. Non-UK nationals or UK citizens working in EEA countries may qualify for refunds under double taxation agreements. For instance, Marta, a Polish graphic designer, worked in London for 6 months in 2024/25, paying £1,500 in Class 1 NI. After returning to Poland, she reclaimed £1,200 under EU rules by proving her Polish social security contributions. Contact HMRC’s International Tax team and provide foreign employment records.

How Does Overpaying NI Affect Your Tax Return?

Here’s something many miss: NI overpayments can tie into your income tax return, especially for the self-employed. If you overpay Class 4 NI through Self Assessment, HMRC may automatically adjust your tax bill. However, don’t count on it—always review your Self Assessment calculations. In 2024/25, HMRC corrected 320,000 Self Assessment NI errors, saving taxpayers £140 million (GOV.UK data). Use HMRC’s online calculator to double-check your figures before submitting.

Can You Claim NI Refunds for Voluntary Contributions?

So, what if you’ve paid voluntary Class 3 NI (£17.45/week in 2026/27) to boost your State Pension? You can claim a refund if you’ve paid unnecessarily—say, if you already have 35 qualifying years. Check your NI record on GOV.UK first. For example, Eirlys, a retired teacher, paid £906 in Class 3 NI in 2023/24, not realising she’d maxed out her pension entitlement. She reclaimed the full amount after contacting HMRC.

Summary of the Most Important Points

You can claim back overpaid NI if you’ve paid too much due to multiple jobs, post-State Pension age deductions, or incorrect tax codes.

Overpayments often occur because NI is calculated per pay period, not annually, leading to errors in complex work setups.

Eligible claimants include employees with multiple jobs, self-employed individuals paying Class 4, and those over 66 still paying NI.

Use your Personal Tax Account, P60, or payslips to verify overpayments against 2026/27 thresholds (£12,570–£50,270 at 8%, 2% above).

Claim refunds using forms CA5610 (multiple jobs) or CA8480 (post-State Pension age), submitting evidence like payslips and bank details.

Non-UK nationals or those leaving the UK may qualify for refunds under double taxation agreements, with proper documentation.

Refunds take 6–12 weeks to process, with delays up to 16 weeks for complex cases like international claims.

Prevent overpayments by applying for NI deferment (form CA72A) or ensuring correct tax codes, especially if over 66.

You can claim refunds for up to 6 years back (e.g., 2019/20 claims are valid until 5 April 2026).

Overpaying voluntary Class 3 NI doesn’t boost your State Pension if you already have 35 qualifying years—check your NI record first.

How a Tax Accountant Can Help You Claim Back Overpaid National Insurance

Navigating the complexities of the UK tax system, particularly when it comes to National Insurance (NI) contributions, can be a daunting task for both individuals and businesses. Overpayments occur for various reasons, including incorrect categorisation, changes in income, or simply due to administrative errors. When faced with such situations, the expertise of a tax accountant can be invaluable. This article explores how a tax accountant can assist you in reclaiming overpaid National Insurance in the UK, shedding light on the procedural, advisory, and strategic benefits they offer.

Identifying Overpayments

A tax accountant begins by conducting a thorough review of your financial history, employment status, and National Insurance contributions to identify potential overpayments. Their understanding of the different classes of NI contributions and the intricacies of the UK tax system allows them to spot discrepancies that you might overlook.

Navigating the Claims Process

Once an overpayment is identified, the process of claiming a refund from HM Revenue & Customs (HMRC) can be complex and time-consuming. A tax accountant can navigate this process on your behalf, ensuring that all necessary documentation is accurately prepared and submitted. They understand the language and requirements of HMRC, enabling them to communicate effectively and expedite the claims process.

Providing Expertise on Legislative Changes

Tax legislation in the UK undergoes frequent changes, which can affect how National Insurance contributions are calculated and refunded. Tax accountants stay abreast of these developments, ensuring that any claim for a refund is based on the most current laws and regulations. This expertise is particularly beneficial in light of recent legislative adjustments affecting NI rates and classifications.

Maximising Your Refund

A tax accountant doesn't just ensure you reclaim what you've overpaid; they also explore opportunities to maximise your refund. This could involve identifying additional overpayments or tax relief opportunities you weren't aware of. Their objective is to optimise your financial position while ensuring compliance with UK tax laws.

Avoiding Future Overpayments

Beyond securing a refund, a tax accountant can provide advice and strategies to avoid future overpayments. This might include recommendations on adjusting your tax code, changing your payment class if you're self-employed, or other financial planning tactics tailored to your specific situation.

Resolving Complex Cases

In cases where overpayments span multiple tax years or involve complicated employment scenarios, the expertise of a tax accountant becomes even more critical. They have the experience to handle complex queries and negotiations with HMRC, providing a level of representation and advocacy that is difficult to achieve on your own.

Offering Peace of Mind

Perhaps one of the most significant benefits of engaging a tax accountant is the peace of mind it brings. Knowing that a professional is managing the process, adhering to deadlines, and acting in your best interest allows you to focus on your personal and professional life without the added stress of tax issues.

Continuous Support

A tax accountant's support doesn't end with a successful claim. They offer ongoing advice and services to ensure your tax affairs are in order, providing regular updates on any changes in tax legislation that might affect you. This proactive approach can help safeguard against future issues with overpayments.

In the labyrinth of UK tax laws and regulations, a tax accountant serves as a valuable guide, especially when it comes to reclaiming overpaid National Insurance. Their expertise not only ensures that you recover what you're owed but also positions you to manage your financial affairs more effectively in the future. Whether through identifying overpayments, navigating the claims process, or providing strategic advice to prevent future issues, the support of a tax accountant can be instrumental in securing your financial well-being in the context of UK taxation.

FAQs

Q1: How can someone check if they’ve overpaid National Insurance without a Personal Tax Account?

A1: They can contact HMRC directly at 0300 200 3500, providing their National Insurance number, payslips, and P60 or P45 forms to verify contributions against the annual thresholds.

Q2: What happens if someone doesn’t claim an NI refund within the deadline?

A2: If the 6-year deadline is missed, they lose eligibility for the refund, and HMRC will not process claims for those tax years.

Q3: Can someone claim an NI refund if they’re still employed by the same employer?

A3: Yes, they can claim a refund if overpayments occurred due to errors like incorrect tax codes or multiple jobs, even if still employed.

Q4: Does overpaying National Insurance affect other benefits like maternity pay?

A4: Overpaying NI does not impact eligibility for benefits like maternity pay, as these depend on qualifying years, not the amount paid.

Q5: Can someone claim an NI refund if they’ve been overcharged due to an emergency tax code?

A5: Yes, an emergency tax code can lead to overpaid NI, and they can claim a refund by contacting HMRC with proof of contributions.

Q6: What is the process for appealing an NI refund rejection?

A6: They can write to HMRC’s National Insurance Contributions Office within 30 days, providing additional evidence like payslips or P60s to support their claim.

Q7: Can someone claim an NI refund if they’ve worked part-time?

A7: Part-time workers can claim a refund if they’ve overpaid due to multiple jobs or incorrect deductions, verified through payslips or HMRC’s NI checker.

Q8: Is there a fee for claiming an NI refund?

A8: No, HMRC does not charge a fee to process NI refund claims.

Q9: Can someone claim an NI refund if they’ve overpaid due to a payroll software error?

A9: Yes, payroll software errors causing overpayments qualify for a refund, provided they submit evidence like payslips to HMRC.

Q10: What should someone do if they’ve lost their P60 or payslips?

A10: They can request duplicates from their employer or use bank statements showing NI deductions to support their refund claim with HMRC.

Q11: Can someone claim an NI refund if they’ve been self-employed for only part of the year?

A11: Yes, if Class 4 or Class 2 NI was overpaid due to partial-year profits or combined with Class 1 contributions, they can claim a refund.

Q12: Does claiming an NI refund affect someone’s credit score?

A12: No, claiming an NI refund has no impact on their credit score, as it’s a tax-related process, not a financial transaction.

Q13: Can someone claim an NI refund if they’re now unemployed?

A13: Yes, unemployed individuals can claim refunds for overpayments from previous tax years, provided they meet the 6-year deadline.

Q14: What if someone overpaid NI due to being on a temporary contract?

A14: Temporary contract workers can claim a refund if NI was overdeducted, especially if tax codes weren’t adjusted for short-term work.

Q15: Can someone claim an NI refund for a deceased relative?

A15: Yes, the executor of the estate can claim on their behalf, submitting relevant documents like P60s and proof of death to HMRC.

Q16: Is an NI refund taxable?

A16: No, NI refunds are not subject to income tax, as they’re a return of overpaid contributions.

Q17: Can someone claim an NI refund if they’ve paid contributions in another country?

A17: They may claim a refund if NI was paid in the UK under a double taxation agreement, but they must provide foreign employment records to HMRC.

Q18: What if someone’s employer refuses to correct an NI overpayment?

A18: They can contact HMRC directly with their NI number and payslips to initiate a refund claim, bypassing the employer.

Q19: Can someone claim an NI refund if they’ve overpaid due to a change in marital status?A19: Marital status changes don’t directly cause NI overpayments, but if tax code errors resulted from the change, they can claim a refund.

Q20: How can someone track the status of their NI refund claim?

A20: They can call HMRC at 0300 200 3500 or check their Personal Tax Account for updates, using their claim reference number.

About the Author

Mr. Maz Zaheer, FCA, AFA, MAAT, MBA, is the CEO and Chief Accountant of MTA and Total Tax Accountants—two of the UK’s leading tax advisory firms. With over 14 years of hands-on experience in UK taxation, Maz is a seasoned expert in advising individuals, SMEs, and corporations on complex tax matters. A Fellow Chartered Accountant and a prolific tax writer, he is widely respected for simplifying intricate tax concepts through his popular articles. His professional insights empower UK taxpayers to navigate their financial obligations with clarity and confidence.

Disclaimer:

The information provided in our articles is for general informational purposes only and is not intended as professional advice. While we strive to keep the information up-to-date and correct, MTA makes no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the website or the information, products, services, or related graphics contained in the articles for any purpose. Any reliance you place on such information is therefore strictly at your own risk. The graphs may also not be 100% reliable.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, MTA cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.