What Can Landlords Claim Against Tax?

- MAZ

- Jul 5, 2024

- 14 min read

Updated: Dec 20, 2025

Understanding Allowable Expenses for UK Landlords

As UK landlords navigate the complexities of tax deductions, understanding what can be claimed against rental income is essential for maximising profitability and compliance. In 2026, several updates and regulations impact what landlords can deduct, shaping financial strategies in property management.

Rental Income and Allowable Expenses

Landlords must calculate their taxable profits by subtracting allowable expenses from their total rental income. Allowable expenses are those necessary for renting out the property and maintaining its condition. Importantly, only expenses incurred wholly and exclusively for the rental business are deductible.

General Maintenance and Repairs:

Expenses for routine maintenance and repairs are typically allowable. These include costs like repainting, fixing broken fixtures, or replacing worn-out elements of the property with similar items. However, improvements that enhance the property's value, such as kitchen upgrades or extensions, are classified as capital expenditures and are not deductible for income tax purposes, though they may be relevant for Capital Gains Tax if the property is sold.

Operating Costs:

Daily operational costs such as utilities, council tax, and insurance (if paid by the landlord), as well as fees for property management services, are deductible. Additionally, landlords can claim expenses for professional fees, including accounting and legal services, directly related to the rental activity.

Travel Expenses:

Costs for travel specifically related to managing the rental property, such as visits for inspections or maintenance, are claimable. However, general commuting or personal travel costs cannot be claimed.

Wear and Tear:

Previously, landlords could claim a wear and tear allowance for furnished properties. This has been replaced by the Replacement Domestic Items Relief, which allows landlords to claim for the cost of replacing furniture, appliances, and other items, as long as the replacement is like-for-like in quality and not an upgrade (GoSimpleTax) (Ross Martin).

Special Considerations for Different Types of Properties

Furnished Holiday Lettings (FHLs):

The Furnished Holiday Lettings tax regime was abolished from 6 April 2025. Holiday lets are now treated as standard rental properties for tax purposes, with no special rules for pension contributions, capital allowances on furnishings, or relevant earnings treatment. Profits are subject to the same rules as other property income.

Limited Company Landlords:

Those who own rental properties through a company are subject to corporation tax rather than income tax. This can involve different forms of relief and requires adherence to specific filing protocols for company accounts and tax returns.

Losses and Property Allowance

Landlords who incur a loss where allowable expenses exceed rental income can carry forward this loss to offset against future profits. This can significantly affect tax payments in subsequent years. For smaller income streams, the Property Income Allowance offers a simplified way to handle taxable income, beneficial for landlords with rental income below a certain threshold.

A Comprehensive List of Expenses that a Landlord May Claim Against Taxes

*HMRC may reject some of these expenses, depending upon your specific expenses

Tax Deductions for UK Landlords - Case Studies and Practical Applications

The tax landscape for UK landlords involves navigating various expenses and deductions to optimise tax efficiency. This section explores practical applications of these rules through case studies, highlighting common scenarios landlords may encounter.

Case Study 1: Renovation and Repair Expenses

Consider a landlord who purchases a property in need of significant repair before it can be rented. The landlord spends money on a new roof, plumbing fixes, and electrical wiring to make the house habitable. According to UK tax rules, these expenses are considered capital expenses because they extend the property's useful life and increase its value. These are not deductible against rental income but may reduce Capital Gains Tax upon the property's sale.

However, if the landlord replaces worn carpets or repaints existing walls without enhancements, these costs are considered allowable expenses because they are necessary for the property's upkeep and do not enhance its inherent value.

Case Study 2: Furnished Holiday Lettings (FHLs)

An owner of a holiday let invests in new furniture and appliances. The expenditure on these items, if similar in quality to the replaced items, qualifies for Replacement Domestic Items Relief (unchanged). However, from 6 April 2025, the abolition of the FHL regime means profits are no longer treated as relevant earnings for pension contributions and no longer qualify for business capital allowances.

Additionally, profits from FHLs are considered relevant earnings for pension purposes, but this will change from April 2025, impacting how landlords plan their tax and pension strategies.

Case Study 3: Property Let Through a Limited Company

A landlord opts to manage their properties through a limited company, thus subject to corporation tax instead of income tax. This structure allows the landlord to claim deductions for the company's operating expenses, such as office supplies and corporate tax advisory fees, which would be different from personal income tax deductions.

Losses incurred in this setup can be carried forward to offset future profits, potentially reducing the company's tax liability in profitable years. This illustrates the strategic tax planning that can benefit corporate landlords.

Property Income Allowance

For landlords with relatively low rental income, the Property Income Allowance offers a straightforward benefit. Suppose a landlord earns £1,200 annually from renting a garage but incurs £500 in expenses related to this rental activity. By electing the Property Income Allowance, they can avoid declaring the full rental income and instead only declare the profit above the £1,000 allowance, resulting in taxable income of £200.

Strategic Planning for Tax Efficiencies and Future Considerations for UK Landlords

In the ever-evolving landscape of property management, staying abreast of tax regulations and planning for future changes are pivotal for UK landlords. This section will explore strategic tax planning tips and upcoming regulatory changes that could impact landlords in the near future.

Strategic Tax Planning for Landlords

Effective tax planning is crucial for maximising profitability and minimising tax liabilities. Here are some strategies that landlords might consider:

Utilizing Losses:

If expenses exceed rental income, resulting in a loss, this loss can be carried forward to offset future profits. This strategy ensures that in more profitable years, the tax burden can be significantly reduced, promoting better financial management over time.

Optimising Property Allowance:

For landlords with rental incomes just above the lower threshold, optimising the use of the Property Income Allowance could result in substantial tax savings. By electing this allowance, landlords can simplify their tax affairs and potentially reduce taxable income.

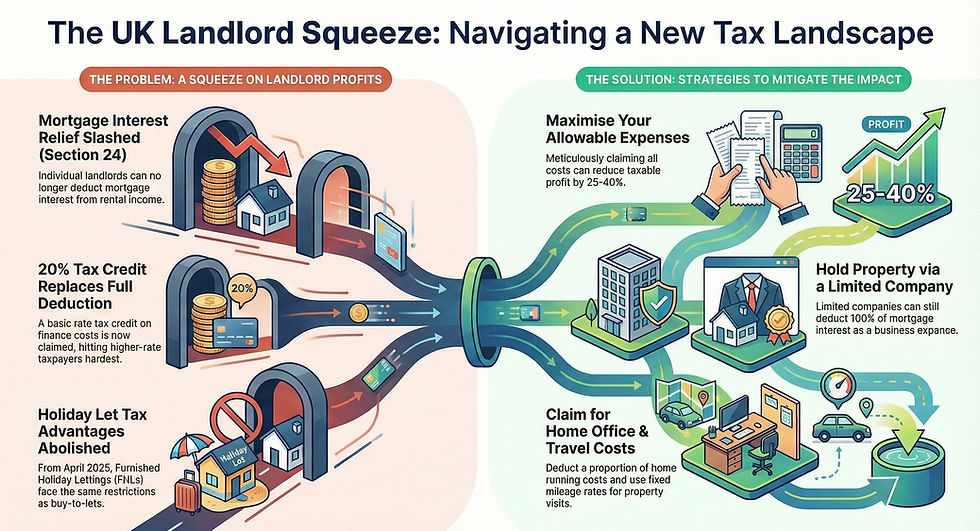

Reviewing Mortgage Interest Restrictions:

Understanding the implications of mortgage interest restrictions is vital. Landlords can no longer deduct mortgage expenses from rental income but may receive a tax credit, which helps mitigate the financial impact. This calls for a review of financing strategies to adapt to these tax changes effectively.

Capital Expenditure Planning:

While improvements and enhancements are not deductible against rental income, planning capital expenditures in a way that maximises potential Capital Gains Tax reliefs upon the sale of the property can be beneficial. Keeping detailed records of these expenditures is crucial for claiming any possible relief.

Regulatory Changes on the Horizon

Several upcoming changes are poised to affect landlords:

Capital Gains Tax Adjustments:

The rates for Capital Gains Tax on the sale of residential properties have been adjusted. For higher-rate taxpayers, the rate has decreased, which might affect decisions regarding the timing of selling properties to optimise tax liabilities.

Changes to Furnished Holiday Lettings:

From 6 April 2025, the Furnished Holiday Lettings regime was abolished. Holiday let profits are now taxed as standard property income, no longer counting as relevant earnings for pension relief or qualifying for business asset disposal reliefs in most cases.

New Tax Regime for Non-UK Domiciled Individuals:

The non-domicile remittance basis was abolished from 6 April 2025 and replaced with a residence-based regime (4-year foreign income/gains relief for new arrivals after 10+ years non-residence). Landlords previously using the remittance basis should review their current tax position under the new rules.

Understanding and navigating the tax deductions available to landlords in the UK requires meticulous planning and up-to-date knowledge of tax laws. By employing strategic tax planning and staying informed of regulatory changes, landlords can optimise their financial outcomes. The upcoming changes in 2025 will necessitate a review of current practices and potentially significant adjustments in how rental businesses are structured and operated. As always, professional advice is recommended to navigate these complex scenarios effectively, ensuring compliance and optimising tax efficiency.

Upcoming Changes to Property Income Tax Rates (from 2027) At Budget 2025, new dedicated Income Tax rates on property income were announced: from April 2027, basic rate 22%, higher rate 42%, additional rate 47%. This separates property income taxation from other income and may affect landlords' overall tax planning, especially those with mixed income sources. Full details are on GOV.UK.

Case Study of a UK Landlord Claiming Different Items and Services in Taxes

Background:

Meet Eleanor Rigby, a fictional landlord based in Brighton, managing a portfolio of three properties. She's gearing up for her self-assessment tax return for the 2025/26 tax year and aims to ensure she's maximising her allowable deductions while staying compliant with HMRC regulations.

Scenario and Steps:

1. Calculating Rental Income and Expenses:

Eleanor's total rental income for the year from all properties is £36,000. Throughout the year, she incurs various expenses, which she meticulously records to ensure they are accurately reported. These expenses include general maintenance, utility bills paid on behalf of tenants, and property management fees.

2. General Maintenance and Repairs:

One of her properties required significant plumbing work and repainting during the year. These costs are straightforwardly deductible as they are considered repairs, essential for the upkeep of the property and not improving its value.

3. Insurance Premiums:

Eleanor has comprehensive landlord insurance covering building, contents, and loss of rent for all properties, costing her £1,200 annually. Insurance premiums are entirely deductible as they are seen as necessary for protecting her investment.

4. Replacement of Furnishings:

In one property, she replaced an old washing machine and a worn-out bed, costing £800 in total. These replacements are claimable under the replacement of domestic items relief, as they are like-for-like replacements not enhancing the property’s value.

5. Professional Fees:

This year, she also decided to use a property management company, which charged £2,000 for their services, including finding new tenants and handling day-to-day tenant communications. Such fees are fully deductible.

6. Travel Expenses:

Eleanor also claims £500 for travel expenses related to her rental activities, such as visiting properties for inspections or repairs. These are deductible as long as they are solely for business purposes.

7. Calculating Net Profit:

After totaling her expenses of £15,500 and subtracting this from her rental income of £36,000, Eleanor’s taxable rental income is £20,500.

8. Reporting and Paying Tax:

Eleanor uses online accounting software to organise her financial records, ensuring accuracy when reporting to HMRC. She files her self-assessment tax return online, reporting her income and allowable expenses diligently to ensure she only pays the tax due, which is calculated based on her net rental income and personal income tax rate.

Eleanor’s meticulous approach to tracking and claiming allowable expenses ensures she maximises her tax efficiency. By understanding what can be claimed and keeping detailed records, she minimises her tax liability effectively while remaining compliant with UK tax laws.

How a Landlord Tax Accountant Can Help You Deal With Landlord Tax

Navigating the complexities of landlord taxes in the UK can be a daunting task, especially given the frequent updates to tax regulations and the intricacies involved in property investment. This is where a landlord tax accountant comes into play, offering invaluable assistance to ensure compliance, optimise tax savings, and streamline financial management. Here, we explore the varied ways a landlord tax accountant can assist property owners.

Ensuring Compliance with Tax Laws

One of the primary roles of a landlord tax accountant is to ensure that all filings are compliant with current tax laws. The UK's tax system is complex, and missing a single regulation can lead to penalties or audits. Accountants stay abreast of changes in tax legislation, such as adjustments to Capital Gains Tax or alterations in allowable deductions, ensuring landlords meet all legal obligations.

Maximising Tax Deductions and Reliefs

Landlords are entitled to various tax deductions that can significantly reduce their tax liability. An experienced tax accountant will help identify all possible allowable expenses—ranging from general maintenance, professional fees, and insurance costs to more nuanced deductions like wear and tear allowances or replacement of domestic items relief. This comprehensive understanding ensures that landlords claim the maximum allowable deductions, effectively lowering their taxable income.

Strategic Financial Planning and Advice

Beyond yearly tax returns, landlord tax accountants provide strategic advice to help landlords make informed decisions about their properties. This may include advice on the optimal time to buy or sell properties based on current market conditions or tax implications of expanding a property portfolio. Accountants can also provide forecasts and simulations to show potential financial outcomes, aiding in long-term financial planning.

Handling Complex Transactions

For landlords dealing with more complex transactions, such as property development, conversions, or purchasing properties at auction, a specialist accountant is indispensable. These transactions can have significant tax implications, including VAT considerations and stamp duty land tax. A knowledgeable accountant ensures that all aspects of these transactions are handled correctly, avoiding costly mistakes and ensuring tax-efficient investment strategies.

Streamlining Record-Keeping and Reporting

Effective management of a property business requires meticulous record-keeping and reporting. Tax accountants assist in setting up efficient systems for tracking rental income, expenses, and capital gains. These systems are crucial not only for current tax reporting but also for future audits or sales of the property. Accountants often leverage modern accounting software to automate much of this process, saving time and reducing the likelihood of errors.

Personalised Tax Advice for Unique Situations

Every landlord's situation is unique, influenced by their specific properties, financial goals, and personal circumstances. Landlord tax accountants offer tailored advice, considering factors like the landlord’s other income streams, residency status, and long-term financial goals. For instance, they can guide whether to own properties personally or through a limited company, each having different tax implications.

Assistance with Tax Disputes and Audits

In the event of a tax dispute or an HMRC audit, having a seasoned tax accountant is invaluable. They can represent landlords during audits, negotiate with tax authorities, and ensure that the landlord’s interests are protected throughout the process. This support can be crucial in resolving disputes efficiently and favorably.

Educating Landlords on Tax Responsibilities

Finally, a crucial role of a landlord tax accountant is education. They ensure landlords understand their tax responsibilities, how different tax rules apply to their circumstances, and how to plan for future tax liabilities. This education helps landlords avoid common pitfalls and manage their finances more effectively.

In conclusion, a landlord tax accountant is a vital resource for managing the intricacies of property taxes in the UK. Their expertise not only ensures compliance and optimises financial outcomes but also provides peace of mind, allowing landlords to focus more on managing their properties and less on the complexities of tax management.

FAQs

Q1: How does the new property income allowance affect landlords with multiple small rental properties?

A: The Property Income Allowance could simplify tax reporting for landlords with several small rental properties, each generating less than £1,000 in rental income. This approach may reduce the administrative burden, as they wouldn't need to declare this income unless total rental income exceeds £1,000 across all properties.

Q2: Are there specific record-keeping requirements for landlords to track allowable expenses and deductions?

A: Yes, landlords need to maintain detailed records of all income and expenditures related to their rental properties. This includes receipts, invoices, bank statements, and mileage logs if claiming for travel expenses. Proper documentation is crucial for supporting claims on a tax return and in case of an HMRC audit.

Q3: Can landlords claim expenses for home office use if managing their rental properties from home?

A: Yes, landlords who manage their rental properties from a home office can claim a portion of their home expenses as business expenses. This includes a reasonable percentage of utilities, property taxes, internet, and phone services, based on the proportion of the home used for business purposes.

Q4: How do changes in mortgage interest tax relief impact landlords with existing mortgages?

A: The changes limit the tax relief for mortgage interest to a basic rate tax credit, affecting landlords with higher incomes more significantly as they can no longer deduct mortgage interest from their income before calculating tax owed. This may increase the tax burden on some landlords.

Q5: What are the implications of the VAT threshold changes for landlords?

A: The increase in the VAT registration threshold may affect landlords who provide services that are VAT-chargeable. It allows more small-scale landlords to avoid the need for VAT registration, simplifying their tax affairs unless their turnover exceeds the new threshold.

Q6: For landlords operating through limited companies, what are the benefits of corporation tax vs. income tax?

A: Operating through a limited company can offer tax efficiencies, such as lower corporation tax rates compared to higher personal income tax rates. It also allows for more flexible planning with dividends and profit retention strategies, potentially resulting in a lower overall tax burden.

Q7: Can landlords claim tax relief on energy efficiency improvements to rental properties?

A: Landlords making energy efficiency improvements may be eligible for various tax reliefs, designed to encourage more sustainable property management practices. These could include deductions or grants available for specific improvements like insulation or energy-efficient boilers.

Q8: What tax implications should landlords be aware of when converting a property into a furnished holiday let?

A: Converting a property into a furnished holiday let can alter its tax treatment, particularly regarding allowable expenses, VAT implications, and how profits are used for pension contributions. Landlords should assess these changes carefully to maximise tax efficiencies.

Q9: How does letting property under a Rent-a-Room scheme affect a landlord’s tax liabilities?

A: Under the Rent-a-Room scheme, landlords can earn a certain amount tax-free from renting out furnished accommodation in their own home. This can significantly reduce tax liabilities if the income received does not exceed the annual threshold.

Q10: Are there any specific tax considerations for landlords who rent to tenants receiving housing benefit or Universal Credit?

A: Renting to tenants on housing benefit or Universal Credit does not alter the tax calculations directly, but landlords must ensure reliable rent collection methods. They may need to consider different strategies for managing payment delays or reductions due to benefit adjustments.

Q11: What are the consequences if a landlord fails to declare rental income?

A: Failing to declare rental income can result in significant penalties and interest on unpaid taxes. HMRC may also conduct investigations, which could lead to further financial penalties or legal action.

Q12: How do recent changes to Capital Gains Tax affect decisions about selling rental properties?

A: Recent adjustments in Capital Gains Tax rates might encourage landlords to sell properties earlier or delay sales, depending on whether the rates are more favorable or not. Planning the timing of sales could significantly impact the tax owed.

Q13: Can landlords claim deductions for security upgrades like CCTV systems?

A: Security upgrades such as CCTV systems are typically considered capital expenses unless they replace existing systems of similar quality. The cost may not be deductible against rental income but could qualify for capital allowances or other tax reliefs.

Q14: Are legal fees related to evicting a tenant tax-deductible?

A: Legal fees incurred for evicting a tenant are generally deductible as they are deemed necessary for managing the rental business. This can include fees for legal advice and court proceedings.

Q15: How should landlords handle tax deductions for properties affected by natural disasters?

A: Landlords can claim deductions for repairs and restorations following natural disasters. These costs are considered part of property maintenance. However, any enhancements or upgrades made beyond simple repairs are treated as capital expenses.

Q16: What are the tax rules regarding landlords receiving rental payments in foreign currencies?

A: Landlords receiving rent in foreign currencies must convert these payments into British pounds for tax purposes using the appropriate exchange rate at the time of the transaction. This ensures accurate reporting of rental income for tax calculations.

Q17: How can landlords utilise capital allowances for commercial properties?

A: Capital allowances allow landlords of commercial properties to deduct the cost of certain fixtures and features from their profits, reducing their tax liability. This includes items like heating systems and security equipment.

Q18: What are the tax implications of leasing property to a business rather than individuals?

A: Leasing property to a business can have different VAT implications and may influence how expenses are deducted. Landlords should consider these factors to ensure compliance and optimal tax treatment.

Q19: Can landlords claim expenses for pest control services?

A: Yes, pest control services are considered a necessary expense for maintaining the rental property's condition and are deductible from the rental income.

Q20: What is the impact of historical listed status on a rental property’s tax deductions?

A: Owning a listed property can affect the types of allowable expenses, especially regarding repairs and maintenance. Specific regulations may govern what changes are permissible, and some expenses may qualify for special tax reliefs due to the property's historical significance.

About the Author

Maz Zaheer, AFA, MAAT, MBA, is the CEO and Chief Accountant of MTA and Total Tax Accountants, two premier UK tax advisory firms. With over 15 years of expertise in UK taxation, Maz provides authoritative guidance to individuals, SMEs, and corporations on complex tax issues. As a Tax Accountant and an accomplished tax writer, he is renowned for breaking down intricate tax concepts into clear, accessible content. His insights equip UK taxpayers with the knowledge and confidence to manage their financial obligations effectively.

Disclaimer:

The information provided in our articles is for general informational purposes only and is not intended as professional advice. While we strive to keep the information up-to-date and correct, MTA makes no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the website or the information, products, services, or related graphics contained in the articles for any purpose. Any reliance you place on such information is therefore strictly at your own risk. The graphs may also not be 100% reliable.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, MTA cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.

Comments