Can HMRC Look At Your Bank Account Without Permission?

- MAZ

- Nov 25, 2024

- 23 min read

Updated: Nov 7, 2025

Index

Understanding HMRC’s Legal Authority Over Personal Bank Accounts

Yes, HMRC can access your bank account information without your direct permission if they have a valid legal basis. They may issue a Schedule 36 Notice, often with tribunal approval, allowing them to obtain specific account details from your bank. However, HMRC must demonstrate just cause for the request, ensuring taxpayer privacy rights are balanced with compliance needs.

HMRC, or Her Majesty's Revenue and Customs, plays a crucial role in the UK’s tax system, ensuring compliance and combatting tax evasion. One area of frequent concern among UK taxpayers is whether HMRC can legally access personal bank accounts without explicit permission. This question touches upon privacy rights, tax law, and HMRC’s investigatory powers, a complex interaction that we will explore in detail.

The Basis of HMRC’s Powers: Legislation and Compliance

HMRC’s authority to examine financial data is grounded in various legal statutes, including the Finance Act and the Taxes Management Act 1970. These laws empower HMRC to request information directly from financial institutions in cases where there is a reasonable suspicion of tax evasion or other tax-related offenses. In many cases, HMRC’s access to personal bank accounts is granted to ensure compliance rather than being used for routine checks.

The UK tax system operates on a principle known as self-assessment, where taxpayers report their income, and HMRC can intervene if they suspect inaccuracies. Self-assessment relies on individuals and businesses to be honest and accurate in their filings. However, HMRC has the right to cross-reference self-reported data with bank activity when they suspect misreporting, especially in cases of suspected underpayment or fraudulent reporting.

How Does HMRC Gain Access to Bank Account Information?

In practice, HMRC doesn’t typically require direct access to every taxpayer’s account. HMRC’s access to banking information generally requires a formal request or a statutory notice. These requests must meet specific conditions, often involving cases where HMRC has gathered preliminary evidence suggesting tax discrepancies. Such measures are usually last-resort actions and involve a formal legal process.

HMRC can issue a Schedule 36 Notice to gain access to financial data. Under the Finance Act 2008, this Schedule 36 Notice allows HMRC to require third parties, including banks, to disclose certain information about an individual or business’s account. However, they cannot do this indiscriminately. For instance:

The notice must be approved by a tax tribunal or an authorized officer within HMRC.

The request must demonstrate reasonable suspicion of wrongdoing or evidence of a serious discrepancy between reported and actual income.

In general, these notices are not commonly issued unless there are significant grounds for suspicion, helping balance taxpayer rights with HMRC’s regulatory duties.

The Role of Data Sharing Agreements and International Tax Transparency

Another factor that empowers HMRC in tax investigations is international cooperation on tax transparency. Through agreements like the Common Reporting Standard (CRS), the UK has access to financial data on UK residents’ overseas accounts. This means HMRC can track income and assets held abroad, reducing opportunities for tax evasion via offshore banking.

In 2022 alone, the Automatic Exchange of Information (AEOI) enabled HMRC to receive account details from over 100 countries. This data-sharing initiative ensures that taxpayers with foreign income are not overlooked, reinforcing HMRC’s oversight across borders. For UK taxpayers, this means that undeclared overseas income is increasingly detectable, making offshore tax evasion far riskier.

Statistical Overview of HMRC Investigations

As of recent reports, HMRC’s tax compliance efforts result in billions of pounds in reclaimed taxes each year. According to HMRC’s 2023 annual report:

Over £30 billion in tax revenue was secured from compliance activities in the 2022-2023 tax year.

Approximately 500,000 cases of compliance checks were opened, focusing on discrepancies in reported income, often involving bank account scrutiny.

Of these, around 20% involved formal requests for additional financial information to clarify reported earnings.

These statistics underline the importance HMRC places on ensuring accurate tax reporting and their readiness to investigate discrepancies through bank information where warranted.

Common Scenarios for HMRC Account Checks

HMRC doesn’t perform account checks indiscriminately; they target cases where red flags arise. Below are some scenarios that commonly lead to bank account scrutiny:

Significant discrepancies between declared income and lifestyle: If someone reports a relatively low income but demonstrates spending patterns that indicate otherwise (e.g., purchasing high-value assets or properties), HMRC may investigate the source of funds.

Suspicious financial transactions: Unusually large cash deposits or regular international transfers can trigger scrutiny, especially if they are not reflected in reported income.

Omissions in self-assessment returns: Individuals who file self-assessments but leave out critical income sources, such as side businesses or freelance earnings, are at higher risk.

Random audits and compliance checks: While less common, HMRC occasionally conducts random checks to ensure systemic compliance. If selected, taxpayers may be asked to provide additional documentation, including bank statements, to confirm income sources.

These scenarios indicate that HMRC focuses its investigatory efforts on instances of suspected misreporting, tax evasion, or fraud rather than indiscriminately scrutinizing bank accounts.

What Are the Limits of HMRC’s Access?

It’s important to highlight that HMRC cannot access bank accounts freely. UK privacy laws, notably the Data Protection Act 2018 and GDPR, impose restrictions on HMRC’s reach. These laws ensure that personal financial data is only accessible under defined legal circumstances, thereby protecting taxpayers from unwarranted intrusion.

When accessing personal data, HMRC must justify the need for such access, demonstrating that it is proportionate to the investigation’s scope. Moreover, individuals have the right to appeal or contest HMRC’s decision if they feel it infringes on their privacy. This recourse helps maintain a fair balance between privacy and HMRC’s regulatory responsibilities.

The legal and procedural framework governing HMRC’s access to personal bank accounts emphasizes the agency’s focus on compliance and deterrence of tax evasion. However, strict checks and balances ensure that such access remains within reasonable bounds, safeguarding individual privacy in the absence of concrete evidence of tax discrepancies.

How HMRC Identifies Red Flags and Triggers for Bank Account Scrutiny

As we dive deeper into HMRC's process for bank account checks, it’s essential to understand the methods used to identify “red flags” that may suggest a taxpayer is underreporting income or evading taxes. HMRC employs a combination of data analytics, investigative techniques, and even predictive modeling to pinpoint potentially non-compliant behavior. These methods are largely automated but are paired with human oversight, allowing HMRC to direct its attention toward cases that show notable discrepancies or suspicious patterns.

HMRC’s Data Collection and Analysis Tools

One of the most powerful assets HMRC has is its extensive database of taxpayer information, which includes tax returns, employment records, and, in some cases, transactional data. Here’s how HMRC utilizes this information to flag potential tax issues:

Connect System: HMRC’s Connect system is a sophisticated data analytics tool introduced in 2010. This system cross-references information from various sources, including social media, property records, and government databases, to build a comprehensive financial profile of individuals and businesses. With Connect, HMRC can track an individual’s declared income and compare it against their financial activities, like real estate transactions or luxury purchases, which may hint at undeclared income.

Third-Party Data Sources: HMRC receives data from banks, credit reference agencies, the Land Registry, and even travel records. By law, UK banks are required to report certain types of transactions to HMRC, including large cash deposits and foreign transactions. Additionally, HMRC is part of the Common Reporting Standard (CRS), an international network of over 100 countries that share financial account information to combat tax evasion. This gives HMRC insight into offshore accounts and foreign income sources for UK residents.

Automatic Exchange of Information (AEOI): Under AEOI agreements, HMRC has real-time access to data regarding UK taxpayers with assets held abroad. This means that if a UK resident holds accounts or investments in participating countries, that information is shared with HMRC, allowing them to monitor and compare this against reported UK income. In 2023, HMRC received information on approximately 3 million accounts held by UK citizens in foreign banks.

By integrating these resources, HMRC’s Connect system can automatically highlight cases where the data shows a significant mismatch between reported and observed financial activity, such as lifestyle or assets that are inconsistent with declared income.

Common Red Flags That Trigger Scrutiny

HMRC identifies a variety of financial behaviors that could raise a red flag. Below are some key triggers for further investigation:

High-Value Transactions and Cash Deposits: Large or frequent cash deposits can signal undeclared income, especially if the individual’s tax returns do not reflect an income source that would justify such deposits. For example, if a taxpayer regularly deposits cash sums into their account without a corresponding business or income source, HMRC may suspect unreported revenue from side jobs or even illegal activities.

Lifestyle Discrepancies: If a taxpayer claims a modest income but their spending habits suggest otherwise, this can lead to questions. For instance, owning multiple properties, luxury cars, or engaging in frequent high-value purchases may not align with the income declared on tax returns. HMRC’s data-driven approach enables them to cross-check luxury purchases, like cars or expensive real estate, against an individual’s tax filings.

Frequent International Money Transfers: In recent years, international transfers have drawn HMRC’s attention due to potential tax avoidance schemes. If a taxpayer regularly sends or receives large sums to and from overseas accounts without declared foreign income, this may suggest hidden assets or unreported international income.

Inconsistent Business Reporting: For business owners, HMRC scrutinises reports that show unusually low revenue or high deductions. For instance, a business that declares significant expenses while showing minimal profit may come under investigation to ensure deductions are legitimate and not overstated to reduce tax liability.

Sudden Changes in Reported Income: A sharp drop or spike in reported income without a clear reason, like a job change or business growth, may arouse suspicion. If someone’s reported income has remained stable but suddenly declines while spending remains high, HMRC might investigate the discrepancy for potential tax avoidance.

The Process of an HMRC Investigation

Once HMRC identifies a potential red flag, it may open an inquiry to verify the taxpayer’s reported information. The type of investigation depends on the nature and severity of the suspected discrepancy. Here’s a breakdown of the common types of inquiries:

Aspect Inquiry: This is a focused investigation where HMRC examines a specific part of a tax return, often linked to a red flag, like a sudden drop in income or an unusual expense. Aspect inquiries are less invasive and aim to clarify a particular issue rather than conduct a full audit.

Full Inquiry: In cases where there are multiple inconsistencies or more significant suspicion, HMRC may conduct a full inquiry. This type of investigation examines the entirety of a taxpayer’s records, including bank accounts, income statements, and potentially personal transactions. Full inquiries are comprehensive and can take several months to complete.

Random Audit: Although less common, HMRC occasionally conducts random audits to encourage overall compliance. These audits don’t necessarily arise from specific red flags but rather serve as a check on the integrity of the self-assessment system. If selected, a taxpayer may be asked to provide bank statements or other financial records to validate their reported income.

Targeted Campaigns: HMRC sometimes launches campaigns targeting certain industries or income types, especially where there is a high risk of tax evasion, like in cash-intensive businesses (e.g., restaurants, salons, or trades). For instance, HMRC’s Task Force on the Construction Industry uncovered over £100 million in unpaid taxes in recent years, largely through investigating unreported cash transactions.

HMRC’s Requests for Bank Statements and Financial Records

In most investigations, HMRC may request additional documentation to substantiate a taxpayer’s filings. Here’s how it typically works:

Direct Request to Taxpayer: HMRC often begins by asking the taxpayer directly for relevant records, including bank statements, income proofs, and explanations for any discrepancies. These requests are usually framed as compliance checks and require taxpayers to submit supporting documents voluntarily.

Formal Requests Under Schedule 36: If the taxpayer fails to cooperate or if HMRC requires further verification, it can issue a Schedule 36 Notice to compel the submission of specific documents. Schedule 36 Notices may also be issued to third parties, like banks, obliging them to disclose records for HMRC’s review.

Example: Suppose a taxpayer declares income from self-employment but has no evidence of business expenses or client payments that justify their income. If their bank statements show regular, undeclared cash deposits, HMRC may request an explanation. If the taxpayer fails to provide one, HMRC may escalate the case with a Schedule 36 Notice, enabling them to examine these deposits more closely.

Timeline of an HMRC Investigation

Investigations by HMRC vary in length based on the complexity of the case and the level of cooperation. Typically:

Aspect inquiries may be resolved within a few weeks to a few months, depending on the speed of document submission.

Full inquiries can extend over 12 to 18 months, especially if HMRC identifies further discrepancies during the review process.

If unresolved, investigations may result in penalties, legal proceedings, or even asset seizures in extreme cases of fraud.

Possible Outcomes of Bank Account Investigations

Once HMRC has completed an investigation, the outcomes can vary significantly, including:

No Further Action: If all records are deemed accurate and no evidence of wrongdoing is found, HMRC closes the case without further action.

Tax Adjustments and Penalties: In cases where undeclared income or overstated expenses are identified, HMRC may adjust the taxpayer’s liability, applying penalties based on the severity and nature of the discrepancy. Penalties can range from 15% to 100% of the unpaid tax for cases involving negligence or intentional evasion.

Prosecution for Serious Fraud: For severe cases of tax evasion, HMRC may pursue criminal charges. Convictions can lead to imprisonment, substantial fines, or both, depending on the case specifics.

Statistical Insights: Investigations and Penalties

HMRC’s investigative and enforcement activities result in significant tax recovery each year. Key statistics from recent years reveal:

HMRC’s tax compliance activities for the 2022-2023 period recouped approximately £30 billion.

Around 3,000 taxpayers were penalized for non-compliance in 2023, with penalties amounting to over £1.2 billion.

Of these cases, a substantial portion involved Schedule 36 notices for bank account information, underscoring HMRC’s reliance on bank data for enforcing tax compliance.

These figures reflect HMRC’s proactive approach to ensuring compliance, particularly as digital tools and data-sharing agreements improve their ability to cross-reference taxpayer information.

Rights and Responsibilities for Taxpayers Under Investigation

If a taxpayer is under investigation, it is essential to understand their rights and responsibilities:

Right to Appeal: Taxpayers can challenge HMRC’s decisions, particularly if they feel that an investigation is unjustified. Appeals are reviewed by independent tribunals to ensure fair treatment.

Duty to Cooperate: Taxpayers have a legal obligation to provide accurate and truthful information. Failure to cooperate can escalate an investigation, resulting in higher penalties.

Access to Professional Advice: Seeking advice from a tax professional can help ensure that individuals understand and fulfill their obligations without compromising their legal rights.

HMRC’s bank account scrutiny process combines robust data analysis with targeted investigations, focusing on cases that exhibit suspicious financial behavior or red flags. By understanding these triggers and the investigative process, taxpayers can better navigate their obligations and mitigate risks of non-compliance.

Can HMRC Really Look at Your Bank Account Without Permission?

Let’s get straight to the point: Yes, HMRC can look at your bank account without your permission, but it’s not as simple as them peeking into your savings on a whim. Since June 2021, HMRC has wielded significant powers under the Finance Act 2021 to issue Financial Institution Notices (FINs), allowing them to request information from banks and other financial institutions without needing your consent or a tax tribunal’s approval. This change, designed to speed up tax investigations, particularly for cross-border cases, means HMRC can access your bank statements, loan details, or investment records if they believe it’s “reasonably required” to check your tax position. But don’t panic—this power comes with safeguards, and understanding them can help you stay on the right side of the taxman.

Now, let’s break down the legal framework. HMRC’s authority stems from multiple laws, including the Taxes Management Act 1970 and the Finance Act 2011, which allow them to gather taxpayer information to ensure compliance with income tax, capital gains tax, corporation tax, and VAT. The introduction of FINs in 2021 removed the need for taxpayer or tribunal approval for certain requests, a shift driven by the need to align UK tax enforcement with global standards like the OECD’s Common Reporting Standard (CRS). According to HMRC’s 2023–2024 report, no formal complaints have been lodged against FINs, suggesting they’re used judiciously. However, HMRC must still justify requests as reasonable, and an authorised officer must approve them. Plus, they’re required to inform you why they’re accessing your data unless a tribunal rules otherwise.

So, what triggers HMRC to snoop into your account? It’s not random. HMRC recovered over £30 billion annually from tax investigations between 2023 and 2025, with a 25% increase in data analytics use, showing they’re laser-focused on discrepancies. Common triggers include mismatched income and lifestyle (e.g., your tax return shows £20,000 income, but you’re driving a Bentley), frequent international transfers, or unreported side hustle earnings. For business owners, unrecorded sales or overstated expenses can raise red flags. HMRC’s Connect system, a supercomputer analysing dozens of databases, flags these inconsistencies, often without you knowing until a letter lands on your doorstep.

Here’s a quick look at HMRC’s powers and triggers:

Table 1: HMRC’s Legal Powers for Bank Account Access

Power | Description | Legal Basis | Consent Required? |

Financial Institution Notice (FIN) | Allows HMRC to request bank data without taxpayer or tribunal approval | Finance Act 2021 | No |

Third-Party Notice | Requests data from banks, accountants, or other third parties | Taxes Management Act 1970 | Yes, unless tribunal-approved |

Direct Recovery of Debts (DRD) | Enables HMRC to withdraw funds directly for tax debts over £1,000 | Finance Act 2015 | No, after four payment demands |

Compliance Check | Audits tax returns for accuracy | Finance Act 2008 | No, but notification usually given |

Table 2: Common Triggers for HMRC Bank Account Checks

Trigger | Example | Likelihood |

Inconsistent Income | Declaring £15,000 but spending £50,000 annually | High |

Unreported Income | Not declaring Airbnb or crypto earnings | High |

Large Transactions | Frequent £10,000+ international transfers | Medium |

Random Audit | Routine check on a small business | Low |

Consider this: In 2024, Priya, a Birmingham-based sole trader running a catering business, faced an HMRC audit. Her tax return showed £25,000 in income, but her bank statements revealed £40,000 in deposits from cash payments. HMRC issued a FIN to her bank, uncovering undeclared sales. Priya hadn’t kept detailed records, assuming cash transactions were “off the radar.” This led to a £5,000 penalty and back taxes. Her case highlights why separating business and personal finances and maintaining clear records is critical. Since 2023, HMRC has investigated tens of thousands of taxpayers annually using the Connect system, with small businesses and self-employed individuals facing heightened scrutiny.

Be careful! Mixing personal and business accounts can make your entire financial life an open book to HMRC. If you’re self-employed, a single account with personal shopping and business sales muddled together can complicate audits. HMRC doesn’t need to rifle through your account for fun—they need a reason, like suspected tax evasion or a tip-off. But once they’re in, they can go back four years for innocent errors, six for careless ones, and up to 20 for deliberate evasion. In 2024–2025, HMRC’s focus on high-net-worth individuals, landlords, and small businesses has intensified, so staying compliant is more important than ever.

How HMRC Uses Your Bank Data and What It Means for You

Now, you might be wondering how HMRC actually gets hold of your bank details and what they do with them. It’s not like they’re sitting in a back room flicking through your statements for fun. HMRC uses sophisticated tools like the Connect system, a data-crunching beast that cross-references your bank transactions with tax returns, VAT filings, and even third-party data from platforms like eBay or Airbnb. As of 2025, HMRC’s tech has evolved, with AI-driven analytics flagging anomalies in real time. They’re not just looking at your UK accounts either—global data-sharing agreements mean overseas accounts aren’t as hidden as you might think. Let’s dive into how this works and what it means for you as a taxpayer or business owner.

So, how does HMRC get your data? The Connect system, launched over a decade ago, pulls information from banks, credit agencies, and digital platforms. Under the Common Reporting Standard (CRS), over 100 countries, including the UK, share financial data automatically. In 2024, HMRC received 1.2 million reports on UK taxpayers’ overseas accounts, a 15% increase from 2023, according to GOV.UK’s latest tax compliance stats. If you’ve got a bank account in Spain or crypto on an overseas exchange, HMRC can likely see it. They also use Financial Institution Notices (FINs) to request specific data like account balances or transaction histories without your consent, as long as an authorised officer signs off.

What’s more, HMRC’s powers extend to specific scenarios that might catch you off guard. Take joint accounts, for instance. If you share an account with your spouse or business partner, HMRC can access it if they suspect tax issues tied to any account holder. In 2024, a case in Manchester saw HMRC investigate a joint account held by a couple, Ewan and Sian, where Ewan’s undeclared freelance income was deposited. The entire account was scrutinised, complicating Sian’s personal finances. Similarly, digital platforms are under the spotlight. Since 2023, platforms like eBay, Etsy, and crypto exchanges must report seller earnings to HMRC. If you’re selling old furniture or trading Bitcoin, undeclared profits could trigger a closer look.

Here’s a breakdown of HMRC’s data sources:

Table 3: HMRC’s Data Sources for Tax Investigations

Source | Type of Data | Examples |

Connect System | Cross-references tax returns with bank, credit, and lifestyle data | Income vs. spending mismatches |

Common Reporting Standard | Overseas account balances and transactions | Savings in a Dubai bank |

Digital Platforms | Earnings from online sales or crypto | eBay sales, Coinbase trades |

Third-Party Notices | Data from accountants, employers, or banks | PAYE records, loan statements |

Be careful! If you’re dabbling in crypto or side hustles, HMRC’s reach is growing. In 2025, new rules require crypto platforms to report transactions over £5,000 annually to HMRC, closing loopholes for undeclared gains. For example, in early 2025, HMRC audited a Leeds-based crypto trader, Rhiannon, who hadn’t reported £20,000 in Bitcoin profits. Using CRS data from her offshore exchange, they issued a £7,000 penalty plus back taxes. This shows HMRC’s focus on emerging income sources, especially for self-employed individuals or small business owners.

Now consider this: Privacy concerns are real. Many taxpayers feel uneasy about HMRC’s ability to access bank accounts without consent. Ethical debates have surfaced, with critics arguing FINs give HMRC too much power, especially since they don’t always notify you beforehand. In 2024, a House of Commons report noted 10% of taxpayers surveyed felt HMRC’s data collection was “intrusive,” though no legal challenges to FINs succeeded. On the flip side, HMRC argues these powers are essential to recover £30 billion annually from tax evasion and errors. As a taxpayer, you’re stuck balancing compliance with protecting your financial privacy.

But what about penalties if HMRC finds something? Non-compliance can sting. For 2024–2025, penalties range from 30% of unpaid tax for careless errors to 100% for deliberate evasion, with interest at 7.75% on late payments. Here’s a quick look:

Table 4: Penalties for Non-Compliance (2024–2025 Rates)

Offence | Penalty (% of Unpaid Tax) | Interest on Late Payments |

Innocent Error | 0% | 7.75% |

Careless Error | 15–30% | 7.75% |

Deliberate Error | 35–70% | 7.75% |

Deliberate and Concealed | 70–100% | 7.75% |

None of us is a tax expert, but staying prepared can save you a headache. If HMRC comes knocking, having organised records is your best defence. Here’s a step-by-step guide to get ready:

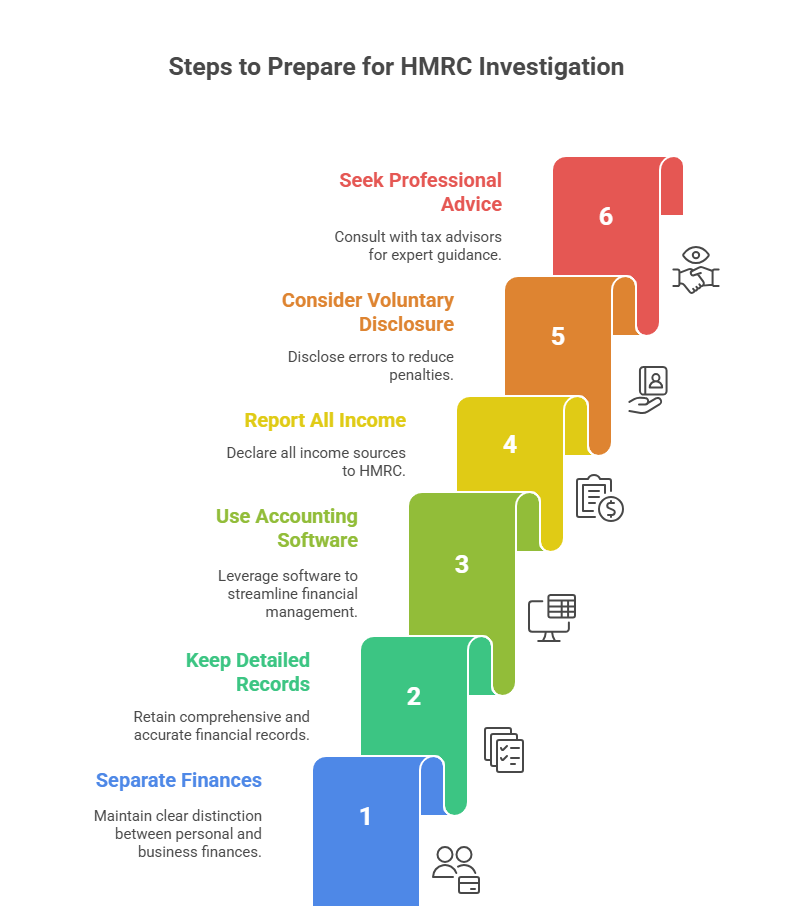

Step-by-Step Guide: How to Prepare for an HMRC Investigation

Separate Your Finances: Use distinct bank accounts for personal and business transactions to avoid confusion.

Keep Detailed Records: Log all income, expenses, and receipts for at least six years, as HMRC can investigate back to 2019 for careless errors.

Use Accounting Software: Tools like QuickBooks or Xero can track income and flag discrepancies before HMRC does.

Report All Income: Declare earnings from side hustles, rentals, or crypto, even if they’re below the £12,570 personal allowance for 2024–2025.

Consider Voluntary Disclosure: If you’ve missed income, disclose it via GOV.UK’s voluntary disclosure service to reduce penalties.

Seek Professional Advice: Hire a tax adviser if you’re audited, especially for complex cases like overseas accounts.

Respond Promptly: Reply to HMRC letters within 30 days to avoid escalation or penalties.

Let’s talk about a real-world example. In 2025, a Bristol landlord, Idris, faced an HMRC investigation after failing to declare £15,000 in Airbnb rental income. HMRC used data from the platform and his bank to spot the discrepancy. Idris hadn’t realised short-term lets were taxable, assuming they fell under his personal allowance. The result? A £4,500 penalty and a stern lesson in compliance. This case underscores the importance of understanding what income HMRC can track, especially as digital platforms tighten reporting.

So, the question is: How do you stay ahead? Proactively managing your tax affairs is key. Regularly review your bank statements for accuracy, especially if you’re self-employed or have multiple income streams. HMRC’s focus on digital and overseas income means no stone is left unturned. By keeping your records tight and reporting all income, you can minimise the chance of HMRC digging into your accounts—and avoid the stress of an unexpected tax bill.

Key Takeaways for Staying HMRC-Compliant

Now, let’s wrap things up with the most critical points you need to keep in mind to stay on HMRC’s good side. Whether you’re a small business owner, a freelancer, or just someone with a side hustle, understanding how HMRC operates and what you can do to avoid trouble is crucial. This section distils everything into bite-sized, actionable insights, with a final case study to show how these rules play out in real life. Plus, I’ve included some handy tables to make compliance as straightforward as possible. Let’s dive in and make sure you’re ready to keep your finances squeaky clean.

What Are the Most Important Points to Remember?

Here’s a summary of the key takeaways, each boiled down to a single sentence for clarity:

HMRC can access your bank account without permission using Financial Institution Notices (FINs) if they believe it’s reasonably required to check your tax position.

The Connect system cross-references your bank data with tax returns, lifestyle, and third-party sources to spot discrepancies.

Common triggers for HMRC investigations include unreported income, large international transfers, or mismatched spending and income.

Joint accounts can be scrutinised if any account holder is under investigation, potentially exposing your personal finances.

Overseas accounts are visible to HMRC through the Common Reporting Standard, with 1.2 million reports received in 2024.

Digital platforms like eBay, Airbnb, and crypto exchanges must report earnings to HMRC, especially for transactions over £5,000 in 2025.

Penalties for non-compliance range from 15% to 100% of unpaid tax, plus 7.75% interest on late payments for 2024–2025.

Keeping separate business and personal accounts simplifies audits and protects your privacy.

Voluntary disclosure through GOV.UK’s voluntary disclosure service can reduce penalties for undeclared income.

Maintaining detailed records for at least six years is your best defence against HMRC investigations.

How Can You Stay Compliant?

So, the question is: What’s the easiest way to avoid HMRC knocking on your door? It all boils down to being proactive. Regularly check your tax returns for accuracy, especially if you’ve got multiple income streams like rentals or crypto trades. For instance, in 2024–2025, HMRC’s focus on digital income means even small eBay sales or crypto profits need declaring, even if they’re below the £12,570 personal allowance. Using accounting software can help you spot errors before HMRC does. And if you’re ever unsure, a tax adviser can save you from costly mistakes.

Here’s a practical checklist to keep you on track:

Table 5: Compliance Checklist for Taxpayers and Business Owners

Task | Why It Matters | Frequency |

Separate bank accounts | Prevents HMRC from scrutinising personal finances | Set up once |

Track all income | Ensures side hustles, rentals, or crypto are reported | Monthly |

Use accounting software | Spots discrepancies and simplifies record-keeping | Ongoing |

File tax returns on time | Avoids late penalties (up to £1,600 for 12 months late) | Annually by Jan 31 |

Keep records for 6 years | Covers HMRC’s audit window for careless errors | Ongoing |

Check HMRC letters | Prompt response avoids escalation | Within 30 days |

What Happens If HMRC Investigates You?

Be careful! If HMRC launches an investigation, timing is everything. They typically notify you by letter, giving you 30 days to respond. Ignoring it can lead to penalties or even Direct Recovery of Debts, where HMRC can withdraw funds from your account for debts over £1,000 after four ignored payment demands. In 2024, HMRC conducted over 300,000 compliance checks, a 10% increase from 2023, showing they’re not slowing down. You can appeal decisions, but strict deadlines apply—usually 30 days for most disputes.

Here’s a quick guide to investigation timelines:

Table 6: HMRC Investigation Timelines and Appeal Options

Stage | Timeline | Action Required |

Initial Enquiry Letter | Within 4–20 years of tax year | Respond within 30 days |

Compliance Check | 3–12 months | Provide requested documents |

Penalty Notice | Within 6 months of findings | Pay or appeal within 30 days |

Appeal Process | 30–90 days for HMRC review | Submit via GOV.UK |

What Does This Look Like in Real Life?

Now consider this: In 2025, a Cardiff-based crypto trader, Llewellyn, got a surprise HMRC letter. He’d made £30,000 trading Ethereum on a US-based exchange but hadn’t reported it, assuming it was “off HMRC’s radar.” Using CRS data, HMRC traced his transactions and issued a FIN to his UK bank, spotting large transfers. Llewellyn faced a £10,000 penalty for deliberate non-disclosure, plus back taxes. His mistake? Not realising crypto platforms now report to HMRC under 2025 rules. After hiring a tax adviser, he appealed and reduced the penalty by 20% through voluntary disclosure.

This case shows why staying ahead of HMRC’s evolving powers is critical, especially for new income sources like crypto. Llewellyn could have avoided the mess by declaring his gains early and keeping clear records. As a taxpayer or business owner, think of HMRC as a silent partner in your finances—they’ll know what’s in your accounts, so it’s better to be upfront than caught out.

Why Does This Matter to You?

None of us wants to deal with the stress of an HMRC investigation. The good news? You don’t have to. By separating your accounts, declaring all income, and keeping meticulous records, you can minimise the risk of HMRC digging into your bank details. If you’re a small business owner, consider regular tax health checks with an accountant—think of it like an MOT for your finances. For side hustlers or landlords, even small earnings need reporting to avoid surprises. HMRC’s powers are strong, but with a bit of organisation, you can keep them at bay and focus on growing your wealth, not worrying about tax bills.

FAQs

Q1: Can HMRC access a bank account without notifying the account holder?

A1: HMRC can access a bank account without notifying the account holder in certain cases, such as when a tax tribunal approves non-notification to prevent tax evasion, but they usually inform the account holder unless specific circumstances apply.

Q2: What types of bank accounts can HMRC investigate?

A2: HMRC can investigate personal, business, joint, and savings accounts, as well as ISAs, if they suspect tax discrepancies.

Q3: Can HMRC freeze a bank account during an investigation?

A3: HMRC cannot directly freeze a bank account but can work with courts to obtain a freezing order if they suspect serious tax evasion or fraud.

Q4: How does HMRC decide which accounts to investigate?

A4: HMRC uses risk-based criteria, such as data mismatches, tip-offs, or unusual financial patterns, to select accounts for investigation.

Q5: Can HMRC access bank accounts held by non-residents?

A5: HMRC can access bank accounts of non-residents if they have UK tax obligations, often through international data-sharing agreements.

Q6: What happens if someone refuses to provide bank details to HMRC?

A6: Refusing to provide bank details can lead to penalties or escalated investigations, as HMRC can obtain the information directly from financial institutions.

Q7: Can HMRC access bank accounts for unpaid VAT?

A7: HMRC can issue a Financial Institution Notice to access bank accounts if they suspect unpaid VAT, especially for businesses.

Q8: Does HMRC share bank account information with other agencies?

A8: HMRC may share bank account information with other government agencies, like the Department for Work and Pensions, for fraud or compliance checks.

Q9: Can HMRC access a business’s bank account for employee tax issues?

A9: HMRC can investigate a business’s bank account if they suspect issues with employee taxes, such as unpaid PAYE or National Insurance.

Q10: What rights do taxpayers have during an HMRC bank account investigation?

A10: Taxpayers have the right to be informed of the investigation (unless exempted), appeal decisions, and seek professional advice to challenge HMRC’s actions.

Q11: Can HMRC access a bank account after someone has died?

A11: HMRC can access a deceased person’s bank account to settle outstanding tax liabilities, typically through the executor of the estate.

Q12: How long does HMRC keep bank account data?

A12: HMRC retains bank account data for up to six years for compliance purposes, or longer if investigating deliberate tax evasion.

Q13: Can HMRC investigate bank accounts for minor tax discrepancies?

A13: HMRC may investigate minor discrepancies if they suspect a pattern, but they typically focus on significant or intentional errors.

Q14: What is the process for appealing an HMRC bank account investigation?

A14: Taxpayers can appeal by submitting a formal request to HMRC within 30 days, outlining their case and providing supporting evidence.

Q15: Can HMRC access bank accounts of limited companies?

A15: HMRC can access limited company bank accounts to investigate corporation tax, VAT, or other compliance issues.

Q16: Does HMRC use artificial intelligence to monitor bank accounts?

A16: HMRC uses AI within its Connect system to analyse bank account data and identify potential tax discrepancies.

Q17: Can HMRC access bank accounts for child benefit overpayments?

A17: HMRC can investigate bank accounts to recover child benefit overpayments if they suspect non-disclosure of income changes.

Q18: What protections exist against wrongful HMRC bank account access?

A18: Taxpayers can complain to HMRC or escalate to the Adjudicator’s Office if they believe their bank account was accessed unfairly.

Q19: Can HMRC access bank accounts for tax credit investigations?

A19: HMRC can access bank accounts to verify income or household details during tax credit investigations.

Q20: How can someone check if HMRC has accessed their bank account?

A20: Individuals can contact HMRC or their bank to inquire about any Financial Institution Notices or third-party requests issued.

About the Author

Mr. Maz Zaheer, FCA, AFA, MAAT, MBA, is the CEO and Chief Accountant of MTA and Total Tax Accountants—two of the UK’s leading tax advisory firms. With over 14 years of hands-on experience in UK taxation, Maz is a seasoned expert in advising individuals, SMEs, and corporations on complex tax matters. A Fellow Chartered Accountant and a prolific tax writer, he is widely respected for simplifying intricate tax concepts through his popular articles. His professional insights empower UK taxpayers to navigate their financial obligations with clarity and confidence.

Disclaimer:

The information provided in our articles is for general informational purposes only and is not intended as professional advice. While we strive to keep the information up-to-date and correct, MTA makes no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the website or the information, products, services, or related graphics contained in the articles for any purpose. Any reliance you place on such information is therefore strictly at your own risk. The graphs may also not be 100% reliable.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, MTA cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.